6 years ago

With the rise of cryptocurrencies in the last few years, also came the increased optimism that billions of the global unbanked population would finally have an inclusive financial solution.

An unbanked person is the informal term for an adult who doesn’t have access to the services of a bank or similar financial organization. It is estimated that there are more than two billion unbanked people in the world, which beget grave effects on individuals and on society. Countries with large numbers of unbanked individuals sustain significant black market economies, and thus tax evasion is prevalent as these individuals work and operate on a cash-only basis. But more importantly, not having a bank account dooms a person to continuous poverty. An unbanked person is unable to save money safely, have access to a pension fund, insurance, or any other type of financial safety net. For women in developing economies, who are 9% less likely to hold a bank account than men, this hurdle creates an even wider gap in gender inequality.

One of the highly anticipated aspirations for Bitcoin in its very early days was that it would be the driving force behind the financial inclusion of the unbanked. By now though it is understood that this process will take longer than initially expected, and will not provide the unbanked with overnight success. Though, happily, in some areas of the world, Bitcoin has been a save in grace. People in countries with failing governments and inexpensive energy for mining - such as Venezuela, use bitcoin religiously. Soaring inflation rates made buying Bitcoin seem like the most solid financial move, despite its high volatility. Another fascinating example is the Bitcoin Beach initiative in El Salvador, where a community was gifted a virtual Bitcoin economy by an anonymous donor, and thus forced to innovate and accelerate financial inclusion. However, in most countries Bitcoin is far too unstable to substitute the local currency. Thus, most unbanked are still left very far from connecting to either the traditional financial ecosystem, or the new one. However, there may be some hope: a certain type of cryptocurrency has developed that might change all that - stablecoins.

Stablecoins are an instrument backed by a reserve asset, e.g. a fiat currency or basket of currencies, cryptocurrencies or other, and thus are designed to keep the value of the asset and prevent volatility of price. One of the largest, USDC has close to $3B in circulation, and is a perfect example of a fully regulated, centralized stablecoin. Another example is Facebook’s Libra stablecoin. Even though it hasn’t been launched yet, it has already spurred numerous governments and central banks to speed up their research and deeply provoked their thoughts concerning the implications such a move would have on Facebook’s 2.7B monthly active users, as well as on the traditional financial system. While centralized stablecoins are controlled by a single entity that manages the reserve, decentralized stablecoins are managed by decentralized organizations that anyone can join. In this instance, decisions are made based on votes of stakeholders and are then carried out automatically through a set of algorithms. Though the underlying technology and economy are indeed complex - they are transparent. Anyone who is willing to put the time and effort into learning them and following decision making procedures, can do so. Due to this transparency, the community has full power to decide which stablecoin are worthwhile, and which are not.

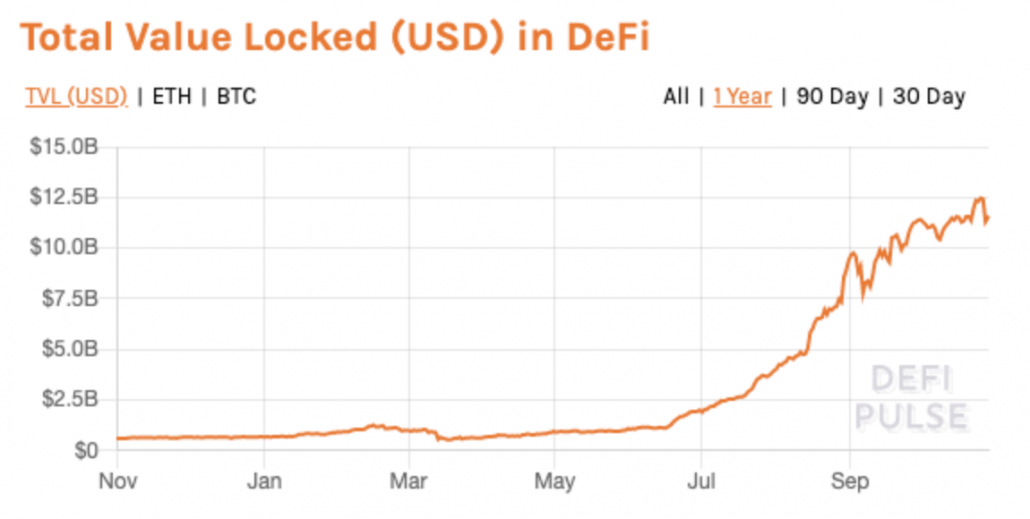

Stablecoins are at the base of the booming decentralized economy (DeFi), growing at about 17X YTD. DeFi tools, or products, are blockchain based applications that allow an advanced set of financial activities. While Bitcoin blazed the trail allowing digital scarcity and P2P transfer of value, Ethereum introduced additional revolutionary features, such as smart contracts and the ability to issue new tokens on top of the network. DeFi applications leverage these features to provide a broader range of opportunities, from borrowing and lending to margin and derivative trading. All of which take place over a decentralized platform and at an unprecedented transparency.

Unlike the traditional financial system, anyone can join and connect to this new system, in some cases even without KYC and without a bank account. These applications can in the future open the door to those who would otherwise not have access to the traditional financial system. In a way, some stablecoins are decentralized banks that allow anyone in - under transparent rules. These products could open new opportunities beyond depositing and saving - say for example free international wire transfers. DeFi can offer an alternative to high transfer fees, which are now estimated at 7% for every dollar a migrant worker sends home. In fact, due to COVID, global remittance payments are projected to fall in 2020 by nearly 20% to $445 billion. Migrant workers sending wages home are the weakest link of society and thus the hardest hit due to the economic crisis caused by the pandemic. This makes every dollar count even more than it had before, and welcomes an upgrade to a more efficient, and less expensive system.

It is far too soon to tell whether DeFi and particularly stablecoins may be the key to helping the unbanked. There are still too many open-ended questions concerning the financial resilience of DeFi and the barriers to entry to mass adoption of stablecoins, centralized or decentralized. On the other hand, if there is one lesson we can learn from Venezuela, or El Salvador’s Bitcoin Beach project, is how agile people can be in looking for and adopting new solutions, when faced with a dire economic situation in which inflation is skyrocketing, or an economy that is in desperate poverty. One thing is for sure, any technology that can make a difference to the unbanked and carry them towards financial inclusion should be taken into serious consideration. It should be carefully examined and validated, as there are no magic pills to solve problems of such magnitude. Sometime in the future DeFi may be just the technological advancement that can make a significant social impact on the unbanked, and hopefully improve the lives of billions, literally speaking.

···

Hexa Foundation is a non-profit organization focused on using blockchain to create social impact. Part of the Orbs Group, Israel’s largest blockchain group, Hexa Foundation aims to use blockchain for social impact, harnessing the technology to help solve the region’s – and the world’s – most pressing humanitarian problems. To learn more visit www.hexa.org.

···

[1] https://www.weforum.org/agenda/2016/05/2-billion-people-worldwide-are-unbanked-heres-how-to-change-this/

[2] https://globalfindex.worldbank.org/

[3] https://www.forbes.com/sites/tatianakoffman/2020/07/14/this-el-salvador-village-adopts-bitcoin-as-money/

[4] Based on USD TVL data (January to end of October) taken from https://defipulse.com/

[5] https://remittanceprices.worldbank.org/en

[6] https://www.worldbank.org/en/news/press-release/2020/04/22/world-bank-predicts-sharpest-decline-of-remittances-in-recent-history

We use cookies to ensure that we give you the best experience on our website. By continuing to use our site, you accept our cookie policy.